A Big Picture Look at the Individual Market

Since the implementation of the Affordable Care Act (ACA) reforms in 2014, the individual health insurance market has changed significantly. A look at these changes yields a few big takeaways:

- The number of issuers declined considerably.

- The types of carriers changed.

- There are large state differences in the magnitude of these changes, which provide insight into some factors affecting market stability.

Data

This analysis used filing data from the Uniform Reporting Rate Template for the years 2014-2017 combined with National Association of Insurance Commissioners (NAIC) reporting data from 2013-2016 available through Mark Farrah Associates. In 2013, carriers with more than 100 enrollees were included. After 2013, the universe for this analysis was limited to carriers who filed Qualified Health Plans (QHPs). The unit of analysis for this study is the issuer in a particular state, rather than an individual plan. For example, an issuer may file 25 plans to sell in a particular state in a particular year, but for this analysis they are counted as one entrant. If a carrier files plans under two separate licenses—as a Health Maintenance Organization (HMO) and also as a health and life insurance company, for example—these entries are counted separately. There is no attempt made here to identify what service areas are covered within the state or whether these service areas changed over time. To the extent possible, plans that were filed but not commercialized were excluded, and every reasonable attempt was made to assure the accuracy of these data, yet it is likely that there are some remaining errors.

Decline in Market Participation

There were 1,041 separate issuers representing roughly 200 parent carriers who participated in the individual market for at least one year between 2013 and 2017. Of these, 35 percent (363) exited after 2013, although some may have continued to renew transitional plans. By and large, these pre-ACA issuers were life or other small insurers that in most states used medical rating and sold more limited plans that were not QHPs. We refer to this class of issuers as “limited coverage specialists.” Another 27 percent (277) of the issuers entered the market in 2014 or after. The parent carriers of these issuers were not necessarily new to health insurance, or even to the individual market, but were new to the individual market in that particular state. Finally, the largest group with 38 percent (401), participated in their state’s market in 2013 and at least one year of the period 2014-2017.

The overall number of issuers in the market was highest in 2013, when there were many limited coverage specialists in most states. There were 764 issuers in total in that year. In 2014, the number of issuers declined sharply, to 440, before rebounding to 609 in 2015, then declining thereafter. Yet while the number of issuers declined, enrollment in the market increased from twelve to roughly eighteen million members. As a result, the average enrollment for issuers in the individual market increased from about 15,000 in 2013 to nearly 34,000 in 2015.

Table 1 shows the pattern of market participation over the time period. By 2017, the number of issuers remaining in the market that had been in the individual market in 2013 had thinned considerably, from 401 to 248.

Change in Issuer Composition

The 2013 individual market was dominated by limited coverage specialists and large national commercial carriers. Together, these two categories accounted for 70 percent of the issuers in the market. But by 2017, considerable change had occurred. The majority of the pre-ACA limited coverage specialists left the market, as did many of the national carriers. And these two categories comprised about 30 percent of issuers. National carriers re-entered the markets in a number of states in 2015, but many had exited again by 2017. While most of the pre-ACA limited coverage specialists exited in 2014, there has been a small resurgence of a new cohort of issuers that specialize in limited coverage but also sell some QHPs. These issuers are not ubiquitous, and usually participate only in the off exchange market in the states where they operate.

As seen in Figure 1, much of the volatility in the market during these years is driven by limited coverage specialists and national carriers. Participation by Blues plans dropped off a bit in 2014, edged up in 2015 and has largely held steady, although at lower levels than in 2013. Regional and provider-sponsored plans increased their participation in the individual market, as did Medicaid Managed Care Organizations. Participation among all these types of issuers peaked in 2015; but 2017 still exceeds 2013 levels. Another very small category, co-ops, had a sharp rise and an equally quick demise, with most having exited the market by 2016.

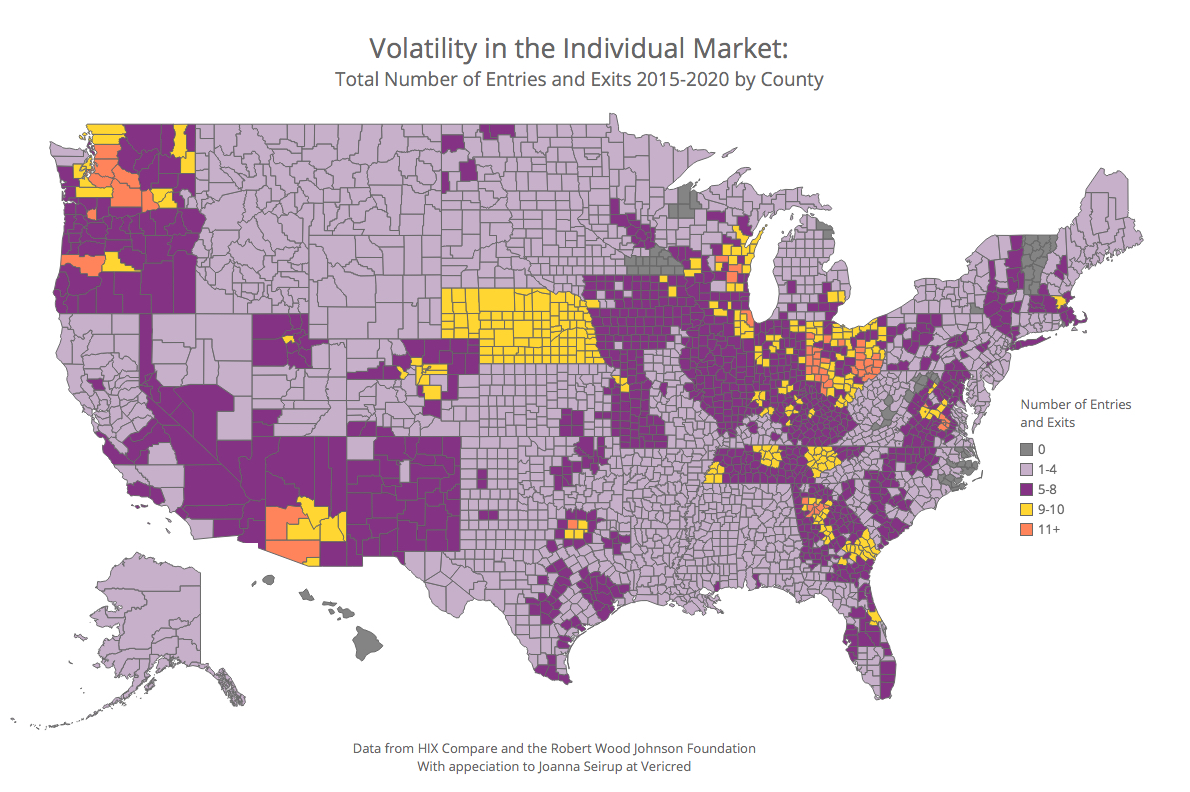

Biggest Losers: Exit Trends in States

These national market trends were not experienced similarly everywhere. A very important differentiating factor is the role of limited coverage specialists in the state coverage landscape pre-ACA. As Figure 2 shows, there was great variation in the relative importance of this type of carrier in 2013 by state, ranging from states where they comprised 80 percent of the market, to those where they were not permitted at all. Predictably, states with more limited specialist carriers in their individual market pre-ACA had more issuer exit. The percentage change in the number of issuers between 2013 and 2017 ranged from more than 80 percent to zero or slight increases in select states as seen in Figure 3.

Exposure to limited coverage specialists pre-ACA also seems to be associated with the number and kind of issuer that participated in state markets after 2014. For example, as seen in Table 2, states with relatively little participation from limited coverage specialists pre-ACA had about two-thirds of their participating issuers in 2015 from the relatively stable categories of Blues plans, regional plans, and provider-sponsored plans. States with high pre-ACA participation from limited coverage specialists, on the other hand, had only about 25 percent of their 2015 issuers from these categories, and instead had nearly two-thirds of their issuers from the national and limited coverage specialist categories. Further, states with little pre-ACA exposure to limited coverage specialist issuers had less issuer exit between the peak year of 2015 and 2017, with a 20 percent decline, as compared with a 45 percent decline for states with the highest share of pre-ACA limited coverage specialists.

The presence of limited coverage specialists in the pre-ACA period seems to be associated with less favorable outcomes for states, although it is hard to say whether the participation of these carriers should be viewed as a cause of market problems or a reflection of deeper structural weakness. Both may be true, since limited coverage specialists tend to flourish in rural states where geography and low population density create certain problems for markets. State variations in insurance regulations may also reflect different approaches to consumer protection. In any case, it would seem that including limited coverage specialists in the individual insurance market helps to create an environment that is not conducive to the attraction or retention of other issuers. Some states continue to permit limited coverage specialists in their market today, as seen in Figure 4. That decision, like the decision to permit transitional plans, contributes to leakage out of the risk pool, and negatively impacts the financial stability of the market for ACA-compliant plans. The magnitude of this impact is an important empirical question.

Related Content