Marketplace Pulse: Are the Markets Ready for the HRA Rule?

The Marketplace Pulse series provides expert insights on timely policy topics related to the health insurance marketplaces. The series, authored by RWJF Senior Policy Adviser Katherine Hempstead, analyzes changes in the individual market; shifting carrier trends; nationwide insurance data; and more to help states, researchers, and policymakers better understand the pulse of the marketplace.

Starting with the 2020 plan year, employers will be able to use Health Reimbursement Arrangements (HRA) to help pay for individual market coverage for their employees. This possibility has generated excitement and some anxiety among market watchers. There is considerable worry about consumer and employee confusion, especially considering the tight timeline for implementation. There are also concerns about the potential for adverse selection, both at the individual and rating area level. On the positive side, some see potential benefits for employers and employees, and a chance for the kind of growth in the individual market that can only come as a result of migration from the much larger group market. Yet, now that this migration is possible, how likely is it? A close look at the markets suggests there are some important differences that may give HRA enthusiasts pause. In most markets, a migrant from the small group market will be asked to pay quite a bit more for a plan which would likely have a smaller provider network, less access to out of network benefits, a different carrier, and higher cost sharing, especially for prescription drugs. While this focus here is on factors relevant to migration from the small-group market, similar considerations would apply to self-insured employer plans.

Here are 5 points to consider:

1. Plan type: likely transition to a closed network

The individual market is known for its narrow provider networks. Additionally, since 2014, the share of individual plans with “open” provider networks–i.e. plans that have out of network benefits–have declined precipitously. The small group market is quite different in terms of plan design. In 2019, 60 percent of small group plans had a point of service (POS) or preferred provider organization (PPO) design, compared with only about a quarter (26%) of individual market plans. Many PPO and POS plans in the individual markets are found in rural areas, where provider scarcity makes it difficult to construct networks. When restricted to large metro areas, the difference between individual and small group plans is more dramatic. Only 15 percent of individual plans have an open network compared with 60 percent of plans in the small group market. It should be noted, however, that in most cases employees in the small group market do not get a choice, while in most counties there is at least some choice in the individual market. This could offset differences in network size and design to some extent.

2. Actuarial value: fewer gold and platinum offerings in the individual market

Another difference between individual and small group market plans concerns metal levels. Not surprisingly, higher metal plans are more common in the small group market, where there are fewer bronze plans (16 percent of small group plans versus 32 percent of individual plans), and more at the gold or platinum level (49 percent versus 27 percent). Platinum plans are far more common in the small group market; they are available in 49 states in the small group market compared with only 18 states in the individual market.

3. Cost-sharing: similar for services, not for drugs

Cost-sharing for health care services is not that different between the small group and individual markets, although differences become larger in gold plans. For example, emergency room visits are subject to the deductible in 70 percent of individual market gold plans versus 52 percent of small group gold plans. Cost-sharing for drugs, however is a different story, as we have previously covered. In the specialty tier, for example, 80 percent of silver plans in the individual market provide no cost sharing before the deductible, compared with approximately half of small group plans. Co-insurance and co-pay amounts differ as well by non-trivial amounts. Enrollees that use specialty drugs will likely notice quite a difference. Overall deductibles are quite similar in the two markets. Median bronze and silver deductibles are a few hundred dollars lower in the small group market, but for gold plans the reverse is true. The median gold deductible is $1,500 in the small group market, versus $1,275 in the individual.

4. Carrier overlap: many will need to switch carriers

Another point to consider is the likelihood of keeping the same carrier. At the state level, a little more than half (53%) of small group carriers also offer individual plans, yet only 23 percent offer individual plans that use the same network. Further, the geography may not be exactly the same. Only 38 percent of state-level small group carriers sell individual plans in all of the same rating areas. Another 14 percent sell individual plans in some of the same rating areas, and the rest sell no individual plans in the state.

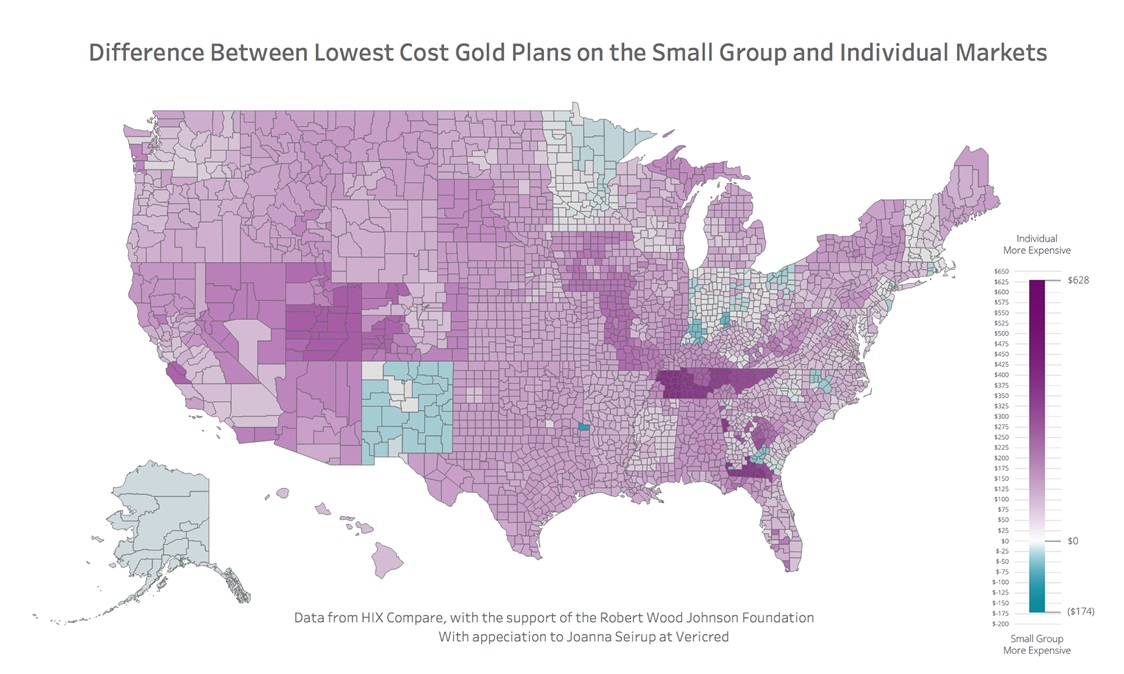

5. Premiums: higher in individual market

In the great majority of states, individual premiums are quite a bit higher. The differences in silver premiums reflect the silver-loading in the individual market. The most pertinent comparison may be gold plans, which are more common than bronze in the small group market. Gold plans are quite a bit more expensive in the individual market, whether measured by the average rating area difference in the cheapest plan (+38%) or the median plan (+18%).

These differences reflect the current characteristics of enrollees in the respective markets. Since most individual market enrollees are subsidized, many plans are designed for lower income consumers and use closed provider networks because they cost less. The risk level in the individual market is also higher, as reflected in the higher premiums and greater cost sharing. This means that the average small group market migrant will be asked to pay more for less generous coverage, and will likely have to change carriers and provider networks. Interest in the HRA rule should be highest in places where the premium differences are relatively low, and carrier overlap is relatively high, such as New Mexico or parts of New England.

Over time, these differences could lessen if enrollees in the two segments become more similar. Carriers in the individual market may begin offering more gold and platinum plans, or otherwise shape benefits. The narrow networks which are typical in the individual market may prove to be inadequate if enrollment increases significantly. Efforts in many states to reduce premiums through reinsurance, cheaper state based exchanges, or potentially public options could increase the competitiveness of the individual market, at least in some states. But in the short run, getting small employers to exercise the HRA option could be a tough sell in many parts of the country, where employers and employees may see little upside from a move to the individual market.

Related Content

Marketplace Pulse: Medicaid Managed Care Organizations in the Individual Market